Gold is reacting to the news today. That’s not the same thing as the gold story changing.

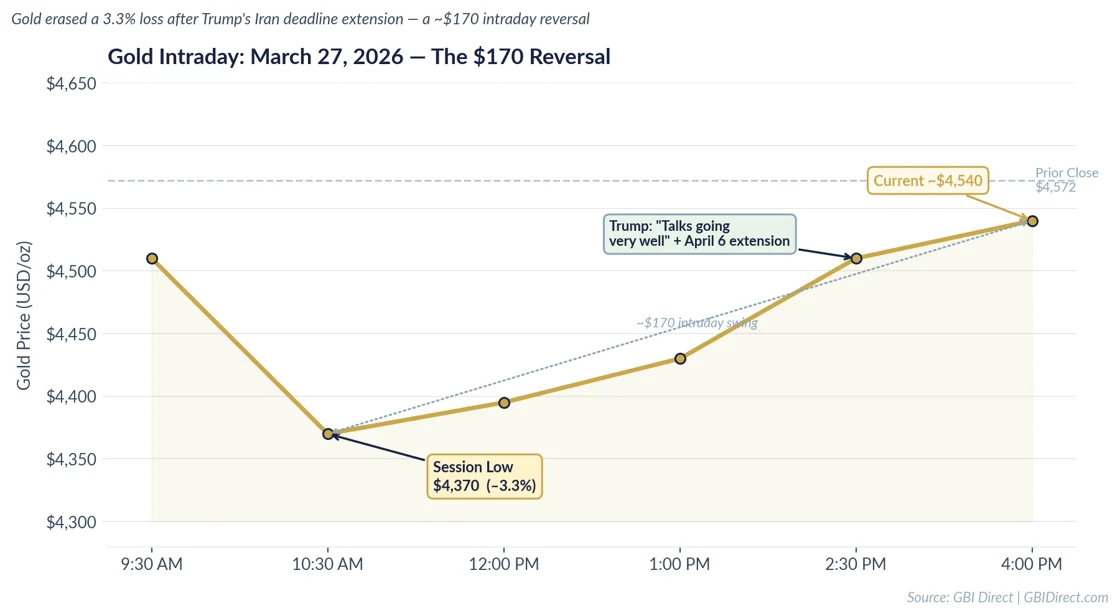

Today’s session told that story in real time. Gold sold off more than 3% to a session low of $4,370 this morning on dollar strength and rising real yields. Then Trump posted on Truth Social that Iran talks are “going very well” — his second extension of the Strait of Hormuz deadline, now set to April 6 — and gold erased every point of that loss, rallying nearly $170 to trade near $4,540. That’s the short-term picture, and it’s real. But it sits on top of a structural case that April 6 cannot touch.

Think about what’s actually been driving gold higher over the past year. It isn’t Iran. It’s the fact that governments around the world are running large deficits, the US dollar has been losing purchasing power, and the Federal Reserve has limited room to raise rates without hurting an already-fragile economy. Those forces don’t disappear based on whether a ceasefire deal gets signed next week. And the biggest investors in the world know it — Q1 ETF inflows into gold hit $21 billion, the second-strongest quarter on record. Central banks are buying at a pace not seen since 2022. Goldman Sachs has a $5,400 year-end target; JPMorgan is at $6,300. That conviction isn’t built on geopolitics. It’s built on something much bigger and much slower-moving.

What April 6 determines is one thing: whether a layer of war premium stays in the price or comes out. The foundation underneath it isn’t going anywhere.

Here’s what’s actually driving gold right now.

Why Gold Reversed: The Iran Ceasefire Trade

What started as a sharp 3.3% selloff has turned into one of the most significant intraday reversals gold has staged this year. From a session low of $4,370, gold has rallied approximately $170 to trade near $4,540 — erasing the entire day’s losses. Gold’s all-time high of $5,595.42 was set on January 29, 2026, and the market remains 21.6% below that peak. But the mechanism behind today’s reversal matters far more than the distance from the high. Two catalysts drove this move, and understanding them separately is how you read it correctly.

This morning, gold was crushed by a rising real yield environment. With the 10-year Treasury at 4.46% and TIPS-implied real yields at approximately 2%, bond markets are signaling higher-for-longer interest rates. In a world of 2% real returns available in risk-free Treasuries, gold—which yields nothing—becomes less compelling. That’s why gold fell hard early in the day. But then the Iran news shifted the entire framework.

Reports emerged that US and Iran negotiators were engaged in talks through Pakistani intermediaries, with ceasefire hopes beginning to circulate in market commentary. If ceasefire speculation gains traction, oil prices fall, inflation expectations ease, and bond markets might price in a softer Fed path. Softer Fed = lower real yields = gold becomes more attractive. That’s the transmission mechanism that drove the $70 reversal. The S&P 500 fell 1.74% and the VIX climbed to 27.44, reflecting broad uncertainty—but gold’s rally within that selloff shows that a specific subset of investors repositioned on geopolitical relief.

The afternoon leg of the rally has a specific catalyst: Trump posted on Truth Social that “Talks are ongoing and, despite erroneous statements to the contrary, they are going very well,” announcing his second extension of the Strait of Hormuz deadline to April 6, 2026. Markets took this as a meaningful de-escalation signal. But the critical detail: Iran has publicly rejected the US 15-point peace framework as “maximalist and unreasonable,” according to Al Jazeera, and Tehran denies it is in direct talks with Washington. The gap between Trump’s framing and Iran’s public posture is significant. This is not a ceasefire. It is ceasefire speculation — and the market is pricing in hope, not a signed agreement.

The Ceasefire Paradox: Why Peace Isn’t Simply Bullish for Gold

Most retail investors operate under a simple heuristic: war = gold up, peace = gold down. That’s incomplete thinking, and it’s about to be tested over the next 10 days.

Yes, a ceasefire removes the geopolitical risk premium—that’s bearish for gold. But simultaneously, a ceasefire eases oil prices, which lowers inflation expectations, which opens the door for Fed rate cuts, which lowers real yields, which is bullish for gold. The net effect is ambiguous. Investors riding gold up purely on “conflict = inflation = gold rallies” are about to encounter a more textured reality.

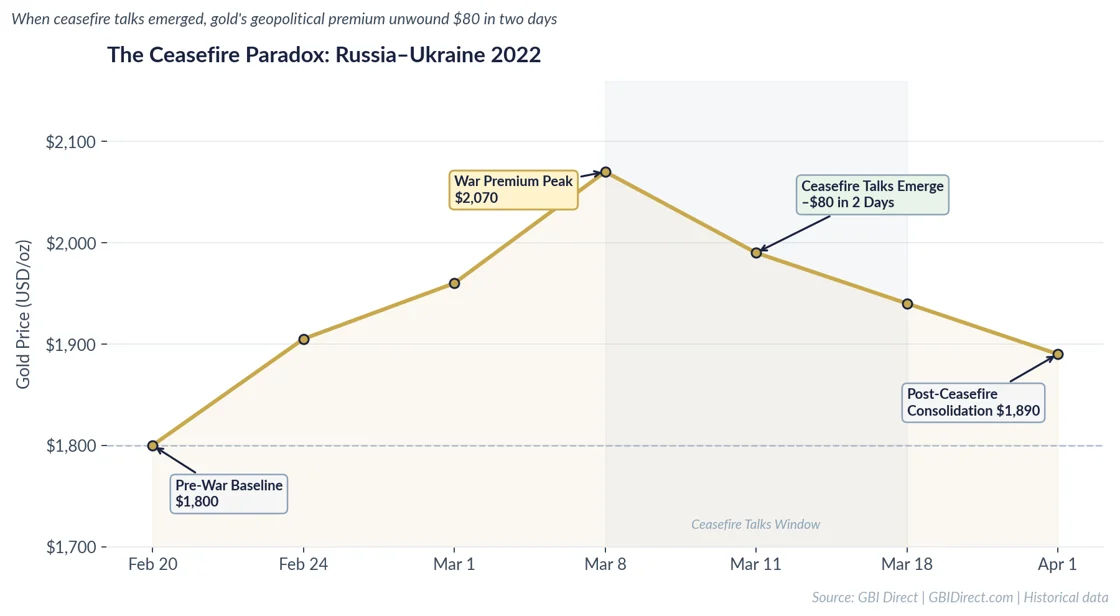

History provides a precise parallel. During the Russia-Ukraine ceasefire talks in early March 2022, gold fell approximately $80 in two days. Gold had rallied to approximately $2,070 on war fears, but when ceasefire negotiations emerged—even though they ultimately failed—the geopolitical premium unwound faster than the rate-cut premium could take hold.

April 6 — Two Scenarios for Gold

With 10 days until the Trump administration’s Strait of Hormuz deadline, the market faces a genuine binary outcome.

Scenario 1: Ceasefire agreement: Gold likely sees a two-phase move. Phase 1: initial relief rally as geopolitical premium unwinds and oil falls, pushing rate-cut expectations up. Gold could trade into the $4,600–$4,800 range near-term. Phase 2: consolidation as the traditional ceasefire paradox reasserts itself and the medium-term path depends on what the Fed actually does with inflation data.

Scenario 2: No deal, escalation continues (higher probability given Iran’s rejection of current US terms): The ceasefire hope trade unwinds. Oil spikes on genuine supply disruption fears, inflation expectations surge, and the Fed faces renewed pressure to hold rates higher. A move below $4,000 would extend gold’s drawdown from the all-time high to 28.6%.

Iran’s public rejection of the US framework means the gap between the two sides remains wide. Today’s $170 rally reflects how much geopolitical risk premium had been priced in — and how quickly it can reprice on a single post. But a social media post is not a peace deal. Watch how gold behaves overnight and into next week: sustained strength above $4,500 would signal the market is pricing meaningful deal probability; a fade back toward $4,400 would confirm this as a tactical repositioning trade.

What Gold Investors Should Watch

PCE Inflation Data (Tomorrow, March 28): The inflation metric the Fed watches most closely. Hotter-than-expected = higher yields = headwind for gold. Cooler = validates rate-cut expectations = supportive for gold.

Nonfarm Payrolls (April 3): Labor market strength affects Fed rate expectations directly. Stronger NFP = lower rate-cut odds = headwind. Softer NFP = higher rate-cut odds = support.

The April 6 Iran Deadline: The binary. Deal or no deal, this date resets the geopolitical calculus and will trigger significant repositioning across commodities, equities, and bonds. Goldman Sachs projects year-end 2026 gold at $5,400; JPMorgan at $6,300. The April 6 outcome will determine whether either target remains credible.

- Gold staged a $170 intraday reversal — from a session low of $4,370 to around $4,540 — after Trump announced a second extension of the Iran deadline and said talks are “going very well.” The move erased the day’s losses and reflects a geopolitical risk premium repricing, not a structural shift.

- The ceasefire paradox: peace removes the geopolitical risk premium that has supported gold, but also eases oil prices and opens the door to Fed rate cuts. The net effect is ambiguous, as seen during the Russia–Ukraine situation in March 2022 when gold dropped $80 in two days.

- The April 6 deadline is a genuine binary event. A ceasefire could push gold toward $4,600–$4,800 in the near term via rate-cut repricing, while escalation could drive prices below $4,000 as inflation concerns resurface.

- Key data to watch: PCE inflation (March 28), nonfarm payrolls (April 3), and April 6 developments. Transmission mechanisms — real yields, the dollar, and oil — matter more than the direction of geopolitical headlines.