The silver market has recorded a structural supply deficit for four consecutive years. The 2026 shortfall is projected at 46.3 million ounces. Here is why the supply side cannot respond — and what it means for long-term investors.

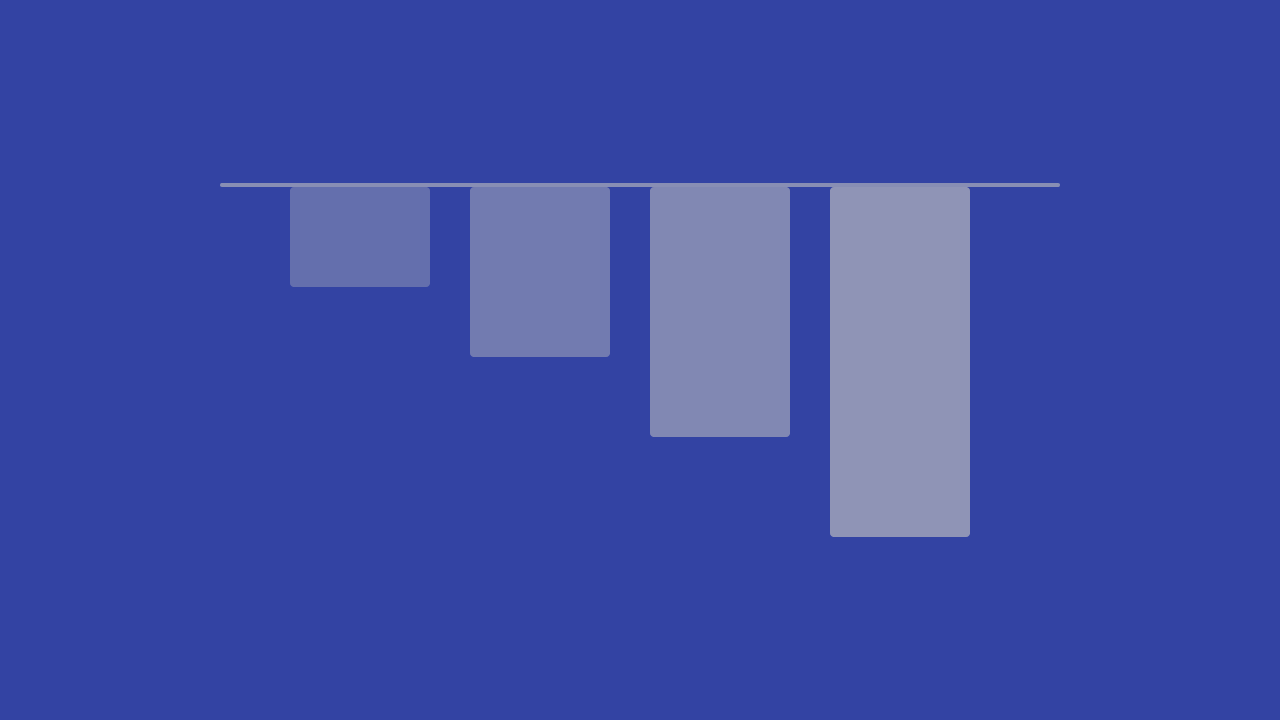

Annual silver supply deficit

A supply deficit that compounds annually

A supply deficit means the world is consuming more silver than it is mining. The difference is made up by drawing down above-ground stockpiles. The Silver Institute has recorded four consecutive annual deficits through 2024 — a cumulative draw of approximately 444 million ounces, equivalent to more than half a year of global mine production. The projected 2026 shortfall is 46.3 million ounces.

Silver supply deficit — million ounces per year

Four consecutive years of structural shortfall. Source: Silver Institute.

Source: Silver Institute World Silver Survey 2024/2025. 2026 = Silver Institute projection. Cumulative 2021–2024: ~444M oz.

70% of silver cannot respond to silver price signals

Approximately 70% of the world’s silver is extracted as a byproduct of mining for copper, lead, and zinc. Production decisions at these mines are governed by the economics of those base metals — not silver prices. The remaining ~30% comes from primary silver mines, which require five to eight years from discovery to production. There is no supply sprint available.

Silver supply — where it comes from

Most silver cannot respond to silver price signals. Source: Silver Institute.

Source: Silver Institute. Approximately 70% byproduct of copper, lead, and zinc mining. ~30% from primary silver mines.

Solar PV, EVs, and data centres — all structural, none cyclical

Silver’s industrial demand is growing structurally — driven not by economic cycles but by the long-term buildout of clean energy and digital infrastructure. Solar PV consumed 197.6 million ounces in 2024, representing 19% of total global silver demand (up from 5% in 2014). EVs use significantly more silver than internal combustion vehicles. And data centres running AI infrastructure require silver’s conductivity at ever-increasing scale.

Silver industrial demand by end use — click to filter

Solar PV is now the largest single industrial end use. Source: Silver Institute.

Source: Silver Institute World Silver Survey 2024. Total industrial demand: 680.5 million ounces.

The structural imbalance between a demand base growing at the pace of the global energy transition and a supply base that cannot respond is not a short-term trading thesis. It compounds annually — and the compounding has been running for four years.

Above-ground stockpiles are drawing down — and the market is noticing

Supply deficits in commodity markets manifest in predictable ways: above-ground inventories decline, lease rates rise as physical metal becomes harder to borrow, and eventually prices respond to reflect the tighter availability. The silver market has been showing these signals consistently since 2021.

Exchange inventories — silver held in COMEX and LBMA-registered vaults — have declined materially over the past four years as the cumulative deficit draws down above-ground stocks. The Silver Institute estimates that cumulative drawdowns since 2021 exceed 444 million ounces — equivalent to more than half a year of global mine production that has been consumed in excess of supply and has not been replaced. That is a stock that, once drawn, takes years to rebuild.

It is worth noting that the silver market is not in immediate physical crisis — above-ground stocks remain substantial and the market functions normally. The point is structural and directional: the buffer is shrinking annually, the forces driving the deficit are growing, and the supply side has no mechanism to respond at the pace required. These are the conditions under which persistent deficits eventually translate into price signals that are durable rather than temporary.

Can recycling close the gap? The honest answer.

The obvious counterargument to the deficit thesis is recycling: as silver prices rise and above-ground stocks accumulate in deployed solar panels, EVs, and electronics, shouldn’t recycling eventually provide a significant secondary supply source?

This is a reasonable question, and recycling does matter. Secondary silver supply from recycling currently contributes approximately 200 million ounces per year — roughly 24% of total supply. This is not negligible. But there are two structural limitations that prevent recycling from closing the current deficit gap, at least in the near term.

First, solar panels have a designed lifetime of approximately 25–30 years. The enormous volumes of silver deployed in solar installations over the past decade will not begin reaching end-of-life recycling stages until the mid-2030s at the earliest. The recycling supply from solar is a future story — potentially an important one, but not one that addresses the current structural deficit. Second, the economics of silver recycling from solar panels are more complex than for industrial applications like photography or electronics, where silver concentration is higher and recovery processes are more mature. Until silver prices rise significantly further or recycling technology improves, the economics do not support aggressive solar panel recycling at scale.

The net picture: recycling provides meaningful secondary supply and will grow over time, but cannot meaningfully close a structural deficit driven by accelerating primary industrial demand in the near term.

Four years of deficits — so why is silver down 37% from its high?

If the silver market has recorded four consecutive annual supply deficits, and if industrial demand is growing structurally, why is silver trading at $76 per ounce — down 37% from the January 2026 all-time high of approximately $121? This is the legitimate question that the deficit thesis has to answer honestly, and it is worth doing so directly rather than glossing over it.

The answer is that silver has two distinct demand components that pull in different directions. Approximately 55–60% of demand is industrial — driven by solar, electronics, EVs, and data infrastructure, and structurally growing. The remaining 40–45% is investment and monetary demand — driven by the same macro forces that drive gold: real yields, dollar strength, Fed policy expectations, and investor sentiment toward non-yielding assets. In the current environment, the monetary component is under significant pressure. Zero Fed rate cuts are priced for 2026. Real yields remain elevated. The dollar is firm. These conditions suppress silver’s monetary demand even as industrial demand grows.

The result is a metal whose price reflects the headwinds in one of its two demand components while the other component quietly compounds beneath the surface. The industrial floor is building. The monetary ceiling is depressed. The price is the net result of those two forces in the near term — and it does not reflect what happens when monetary headwinds eventually ease and the structural industrial case reasserts itself at full force.

This is not a permanent condition. Real yields respond to the rate cycle, which responds to economic conditions, which change. The fiscal and debt dynamics of the U.S. economy — deficit at 6–7% of GDP at full employment, total debt exceeding $34 trillion — make sustained high rates economically punishing over a multi-year horizon. When the rate cycle turns, the monetary component of silver demand will recover. And when it does, it will recover against a backdrop of a structural industrial deficit that has been compounding for five or six years.

The three leading indicators that tell you the structural thesis is playing out

For investors who hold silver on the basis of the structural supply deficit, identifying the right indicators to watch is more useful than tracking the spot price on any given day. Three metrics are worth monitoring consistently.

COMEX silver inventory levels. Exchange-registered silver — held in COMEX-approved vaults and available for delivery against futures contracts — is the most transparent measure of readily available above-ground stocks. Persistent drawdowns in registered inventory, sustained over multiple months and across multiple depository locations, are a meaningful signal that the physical market is tightening. This is distinct from spot price moves, which can be driven by paper futures positioning rather than physical supply-demand. When registered inventory drawdowns are accompanied by rising lease rates — the cost of borrowing physical silver — the tightening signal is more reliable.

Annual solar installation data from the IEA and BloombergNEF. The size of the solar deficit in any given year is directly proportional to the volume of solar capacity installed globally. The IEA projects 540 GW of new solar additions per year through 2035. Each year that actual installations come in above that projection — as March’s export data suggests 2026 might — the deficit is larger than the base case. Each year installations disappoint, the pressure is less. Tracking the annual global solar installation figures against projections is the most direct leading indicator for silver’s industrial demand trajectory.

The PERC-to-TOPCon migration rate. The technology transition from legacy PERC cells to TOPCon and SHJ architectures is the multiplier on the volume story. If the industry migrates to TOPCon faster than expected — as early 2026 data from Chinese manufacturers suggests — the silver-per-GW intensity rises even as volumes grow. Quarterly earnings calls from Chinese solar manufacturers (LONGi, JA Solar, Trina) consistently report on cell technology mix. Tracking the share of TOPCon in total shipments is a leading indicator for the silver intensity trend.

- Four consecutive annual supply deficits through 2024. Cumulative draw: ~444 million ounces. 2026 projected shortfall: 46.3 million ounces.

- 70% of silver is mined as a byproduct of base metals — supply cannot respond independently to silver price signals.

- New primary silver mines require 5–8 years from discovery to production — no supply sprint is available.

- Industrial demand is growing structurally: solar PV (197.6M oz in 2024), EVs, and data centres are all expanding.

- Solar industry migrating to TOPCon/SHJ cells requiring 1.5–2× more silver per GW than legacy PERC technology.

- Ghent University projects solar alone consuming up to 41% of total global silver supply by 2030.

Build your silver position before the structural deficit tightens further. GBI Direct offers fully allocated silver storage through Brinks and Loomis vaults — institutional custody, live-market pricing, accounts open in under 10 minutes.

Sources: Silver Institute, World Silver Survey 2024/2025; Ghent University / Cattaneo et al., ScienceDirect (2025); IEA World Energy Outlook; Silver Institute, “Silver: The Next Generation Metal” (2025, Oxford Economics).

Not financial advice. For educational purposes only.